Unlike more complex methodologies, such as double declining balance, this method uses only three variables to calculate the amount of depreciation each accounting period. The straight-line method is one of the simplest ways to determine how much value an asset loses over time. In this method, companies can expense an equal value of loss over each accounting period. The assumption made by accountants is that the asset loses the same value over each period.

What Is Straight Line Depreciation Method?

As $500 calculated above represents the depreciation cost for 12 months, it has been reduced to 6 months equivalent to reflect the number of months the asset was actually available for use. E.g. rate of depreciation of an asset having a useful life of 8 years is 12.5% p.a. This approach calculates depreciation as a percentage and then depreciates the asset at twice the percentage rate. Lastly, let’s pretend you just bought property to build a new storefront for your bakery.

Step 1: Calculate the asset’s purchase price

This consistency and simplicity make it a preferred choice for many businesses. If your company uses a piece of equipment, you should see more depreciation when you use the machinery to produce more business transaction definition and examples chron com units of a commodity. If production declines, this method lowers the depreciation expenses from one year to the next. After building your fence, you can expect it to depreciate by $1,467 each year.

- That’s how we calculate our net book value and this net book value, that’s generally what we show on our balance sheet.

- The straight line method is the easiest way of spreading the cost of an asset over its useful life.

- The assumption made by accountants is that the asset loses the same value over each period.

- While the straight-line method is the easiest, sometimes companies may need a more accurate method.

- It’s a must-read for anyone looking to understand how depreciation affects the value of assets over time and its impact on financial statements.

How does straight line depreciation differ from other depreciation methods?

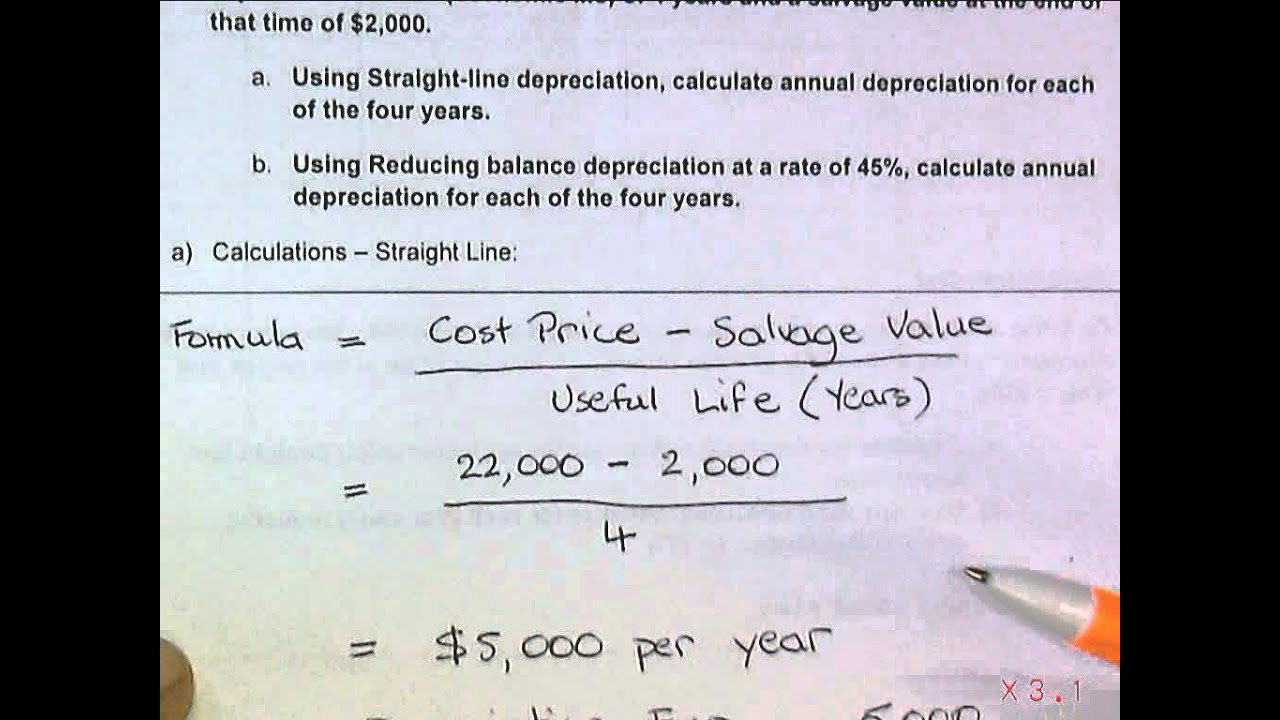

Accountingo.org aims to provide the best accounting and finance education for students, professionals, teachers, and business owners. The last accounting year in which an asset is depreciated is either the one in which it is sold or the one in which its useful life expires. For example, a machine that costs $110,000 with a useful life of 10 years and salvage value of $10,000 will be depreciated by $10,000 each year [(110,000 – 10,000) ÷ 10].

Let’s break down how you can calculate straight-line depreciation step-by-step. We’ll use an office copier as an example asset for calculating the straight-line depreciation rate. The most important difference between this formula and other common depreciation formulas is the denominator. Other methods have a denominator of 1 or 1/2 depending on whether an asset was acquired during its first year or after it had been in use for 1 year. The denominator in straight-line depreciation is 1/ Estimated Useful Life, which has the effect of making 1/ Estimated Useful Life much larger than 1 or 1/2 when an asset is new. Learn about straight-line depreciation and how to apply it when depreciating fixed assets.

In conclusion, the straight line method of depreciation is essential for calculating and reporting allowable depreciation deductions for tax purposes. By following IRS guidelines outlined in Publication 946, taxpayers can ensure they accurately report depreciation expenses and maintain compliance with tax laws. For example, due to rapid technological advancements, a straight line depreciation method may not be suitable for an asset such as a computer. It would be inaccurate to assume a computer would incur the same depreciation expense over its entire useful life. Straight-line depreciation can be recorded as a debit to the depreciation expense account. It can also be a credit to your accumulated depreciation account.

This is machinery purchased to manufacture products for the business to sell. Since the equipment is a tangible item the company now owns and plans to use long-term to generate income, it’s considered a fixed asset. Below are three other methods of calculating depreciation expense that are acceptable for organizations to use under US GAAP. Accumulated depreciation is carried on the balance sheet until the related asset is disposed of and reflects the total reduction in the value of the asset over time.

You installed a fence around the entire plot of land, which falls under the 15-year property life. The initial cost of the fence was $25,000, and you think you can scrap the wood for $3,000 at the end of its useful life. According to the straight-line method of depreciation, your wood chipper will depreciate $2,400 every year. Now that you know the difference between the depreciation models, let’s see the straight-line depreciation method being used in real-world situations.